In insurance broking, managing uncertainty is our bread and butter. It’s our job to take a measured look, and to help our clients respond to eventualities as they emerge. Of course, we can’t offer a helping hand when things go wrong if our own footing isn’t firm. That means having a good idea of what might be coming down the pipe for ourselves … as well as for you.

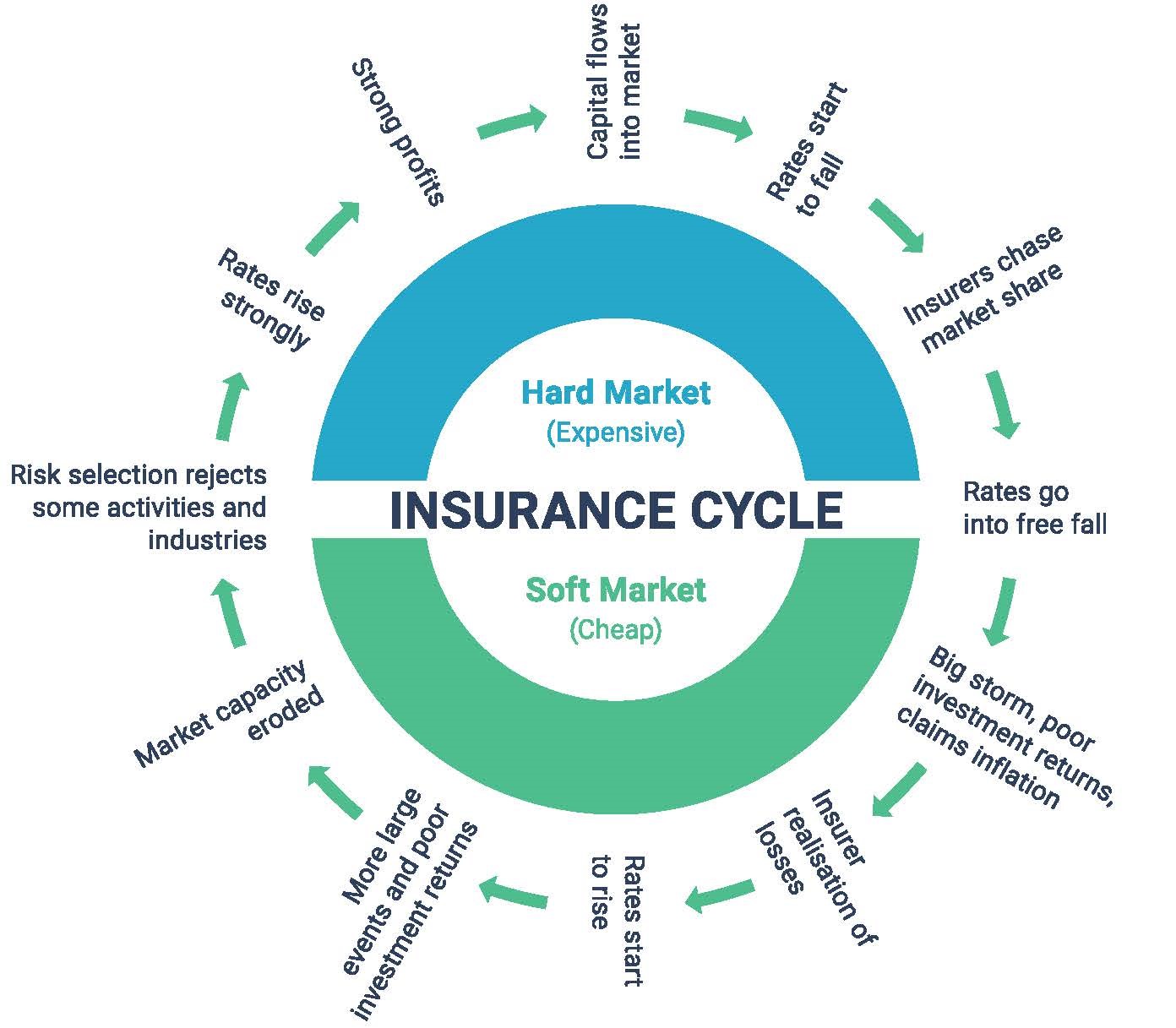

It’s hard to say that the past year has been great for insurance. Profitability took a dive in 2019, and we’re still waiting for a recovery. APRA’s most recent report shows some growth in profitability, but not much. It’s not all bad news, however: I believe we’re at a point in the insurance cycle where the tide starts coming in again. That is, when there is a more equitable relationship between the degree of risk and costs to transfer it in a policy.

How bad is it, Doc?

On the surface, the picture isn’t pretty. The pattern we’re seeing in insurance is one of rates increasing, capacity receding and profitability staying level. Let’s take a look at what’s behind those trends.

Generally, what causes premiums to go up is big losses like we’ve had over the past few years, with economic upsets and natural disasters. These are situations where insurers are suffering the losses, reducing market capacities and moving out of unprofitable markets that they had previously stayed in. It means premiums go up, and it gets harder to access insurance in certain industries and regions.

There was a good report from Fitch Ratings recently that showed how the insurance industry has been affected over the past couple of years. One result of COVID has actually been a decrease in global risk. For example, there are fewer people on the road, less road freight and logistics and fewer people travelling. So, the risks and payouts around motor insurance have gone down and insurers in that sector have been running more profitably.

In other words, COVID has reduced some operating risks and insurers are rebuilding their coffers and doing what they have to do to remain stable and continue offering coverage.

Things are looking up, actuary

Part of the problem with the pandemic, business-wise, has been uncertainty. This has been a particular problem for insurance, because making good predictions is what makes the industry work.

From looking at “Global reinsurance sector position improving” (an article in Insurance Business Australia that quoted the Fitch report), the uncertainty is going down for three main reasons:

Pandemic-related losses have stayed within projections so far

Insurers are responding with COVID-specific language in policies, helping to minimise future payouts and thus protect their ability to offer fairer pricing

Increasing vaccination rates are cutting health and mortality payouts.

It’s good to look at the situation for reinsurers; after all, they assess the risk represented by insurance companies themselves. Good projections for reinsurers reflect a healthy insurance industry. That said, it can take some time for increased profitability and stability to flow downstream to you, the client. For example, Fitch doesn’t expect reinsurance prices to go down in the coming year, which means consumer-facing insurers are not going to see that benefit.

So, when will my premium go down?

You might be asking “if uncertainty is going down, then what?”. I like to think of the insurance cycle as a clock – when you have a major disaster, that moves the hour hand to 4 o’clock. The market then follows a predictable cycle, where you see insurer losses, rising rates and receding capacity. Eventually, insurer profitability returns, leading to an increase in market capacity, stronger profits, price competition and easing of consumer prices.

Anyway, I think we’ve now spun around to about 10 or 11 o’clock. That means we’re seeing continued strongly rising rates, which will be followed by a period of strong profits. For reinsurers, Fitch expects up to a 2 percent rise in combined ratio in the coming year, and again the year after that.

As we’re entering this hard-market part of the cycle, you can expect to see the following:

Premiums will probably continue to rise over the coming 12 months

Getting insurance coverage could become more difficult for many

Negotiating terms will become harder and take considerably longer to facilitate

Until higher profit levels return, insurers will reduce capacity

Higher excesses in general

A greater focus on risk management and mitigation processes

More time and additional information will be required from you before insurers offer coverage.

The coming year or two

The cyclical nature of the insurance market means that costs will eventually stabilise and potentially reduce. However, in the immediate future, coverage costs are likely to go up, or plateau. If you haven’t started to focus on your insurance costs as a major business expense, you need to ask what you can do internally to mitigate these exposures.

First of all, if your insurance broker is doing their job well, it should make things easier for everyone: for you and your insurance company! You should get the right – that is, the most accurate – cover for your operations. As always, seek advice from a suitably qualified risk-management professional on controlling and mitigating your risks.

A recent article titled “Global cyber insurance pricing rises 32%” has led to some interesting conversations at Alleviate Risk among my team, and with the odd client. Why? Because cybercriminals are opportunistic and we’re in a new world of business. The recent haphazard rush to working from home means all manner of cyber vulnerabilities have been created or revealed in businesses across the economy – small, medium and large.

This quote from the article sums it up nicely:

“COVID-19 and all of its attendant effects on technology adoption and cybersecurity, combined with independent or connected changes to the loss environment, has added a big dose of complexity into an already complicated risk landscape.”

That’s from Shay Simkin, head of cyber at international insurance broker Howden. Yes, she is speaking in a US context, but the same trends are happening here.

Think about it. All of a sudden, we’re being forced out of our workplaces, where IT is professionally managed, controlled and monitored, into using our own devices and home internet connections. The risks are clear.

In this context, the degree of difficulty for being a cybercriminal has come way down. Many cybercriminals these days aren’t “genius hackers”, they’re just conmen who’ve downloaded automated security -probing software. That’s all they need to launch the two main kinds of attacks we’re seeing: spoofing and ransomware.

Spoofing: cybercriminals intercept emails and then use social engineering (digital grifting, essentially) to fiddle with invoices to divert money into their accounts.

Ransomware: one day you go to work, switch on the computer and find that your entire business system is encrypted and crippled. All you have is an ultimatum: pay some sort of cryptocurrency amount to a mystery destination or your data will be deleted.

The point is, you and all the other businesses you do business with have been thrust into an era of slapdash cybersecurity. I’ve been working around this a lot, so here are my key insights…

My top 4 points about cybersecurity risks

If you think you won’t get hacked, you’re mistaken. Actually, if you think you are immune, your risk increases. Chances are your site has already today been cased by cybercriminals looking for soft targets. It’s like that story with the two people about to get chased by a tiger and one of them stops to put on running shoes. You don’t have to outrun the tiger, you have to outrun the other guy. The cybercriminals are always coming, so, at a very basic level, your online presence just needs to be too tough to bother with.

Insurance does not bring back data that has been encrypted or lost. Two factors here: highly sophisticated encryption tools are cheap, and decryption or recovery is rarely successful and is always very costly.

You probably won’t get your data back, even if you pay a Bitcoin ransom. Research from Kaspersky has found that only about 25 percent of ransomware attack victims get everything back. After all, the cybercriminals have little incentive to keep their side of the bargain.

Being a cybercrime victim casts your business in a bad light. Regardless of the data loss or outcome, there are major reputation risks associated if you have a data breach. Imagine sending a letter to all your clients saying “we were hacked and your personal data was stolen”. At the very least, this will cost you business. At worst, you could end up in court.

The big effect of raising your cybersecurity bar a little

To handle this emergent situation you must mitigate your cyber risk exposures. The key to doing so rests in how most cybercriminals operate: they cast a wide net and try to scoop up easy pickings. Generally, their automated software scans thousands of sites a day looking for specific weaknesses. If your site doesn’t have them, the scanner moves on. Trust me, your site has been scanned for weaknesses thousands of times already. This means the best cybersecurity mitigation tactic is often simply to be a slightly tougher nut to crack than the next guy.

Yes, you can have cybersecurity as part of your business insurance, but the standard cover is pretty skinny. It’s better than nothing, but you’re far better off with a standalone specific cyber policy that is responsive to your cyber-risk management practices.

Being proactive on cybersecurity goes a long way

My point is that prevention will always be better value for money than paying a Bitcoin ransom. And the tigers are already stalking your online presence, but they usually seek to attack the weaker targets. So, instead of outrunning the tiger, outrun the pack mentality of “cybercrime happens to other people”.

To learn more about “putting on your running shoes”, reach out to someone in your network who can connect you with a cybersecurity expert and/or seek a suitably qualified risk expert to assist you in mitigation strategies. At the very least, have the conversation so you understand where your exposures lay.

If you weren’t watching the insurance news, there was an interesting article recently. And when your insurance broker says “interesting”, you know they mean “concerning”.

The article is on insurancenews.com.au. It is about a presentation that the Insurance Council of Australia (ICA) CEO Andrew Hall gave to the House of Representatives Standing Committee on Economics. The headline: General insurers facing ‘greatest challenge in two decades’.

If that sounds like the hot air that peak bodies often offer up to government committees, you’d be right: it does sound like that. But this is not hot air. This quote from Hall shows why:

“Insurer profitability over the 24 months ending March 2021 was down 64 percent on the preceding two years, and according to APRA the entire general insurance sector only made a profit of $19 million in the most recent March quarter.”

That $19 million is shockingly low. For a multi-billion-dollar sector to be running at a fraction of a percent profit margin is not sustainable. It will not continue. Something will change. Here’s what I think will happen.

First, reinsurance costs will continue to go up as they have been over the past 18 months. This will affect the pricing models that insurance companies work from. In turn, this will have three outcomes: one, it’ll get passed on to customers for certain lines of insurance; two, insurers will simply pack up their bags and stop offering that line of insurance (which we are also seeing in certain product lines); or, three, insurers pricing certain products at a level where it makes the expense borderline unviable for clients (which we are also already seeing).

None of this should be a surprise

As an insurance broker, I’m already seeing all of these effects. When we get enquiries from certain kinds of businesses, it is difficult to find anyone willing to offer insurance at any price. If you read between the lines, you can see Hall saying the same things here:

“We are aware that the availability and affordability of some commercial lines of insurance for small and medium-sized businesses has become challenging.”

If you know business-speak, you know that “challenging” often means “unviable”. What Hall is trying to do is to highlight that these rising insurance premiums are not price gouging: it’s the insurers trying to survive in an increasingly complicated world. A world in which offering insurance against many categories of risk has become increasingly difficult. However, the ability for businesses to manage risk is a necessity in a functional capitalist economy. There are two ways to do it:

Transfer the risk through buying insurance policies

Mitigating the risk through adapting your operations.

Given the continual shocks to the global and domestic sense of “business as usual”, it is becoming clearer and clearer that it makes sense to find a balance between the two.

Transferring and mitigating risk

A common way to start introducing more of Option B into your business is to find a risk-management expert who not only also understands your transactional environment but also understands your business model. They will be able to analyse your exposures and advise on what to do about them. When you implement those actions, you’ll still have some risks left over, of course. And it is these risks – the ones it is uneconomical to mitigate internally – that you then seek to transfer out via more appropriately priced insurance policies.

For most SME businesses – even those at the larger end – risk management and insurance is typically delegated to the Chief Operations Officer or Chief Financial Officer. But do they actually have dedicated risk-management skills? Probably not.

Of course, most businesses don’t have the financial capacity to employ someone specifically to deal with risk, but they can call on someone suitably qualified. Someone who has studied risk management and has the academic credentials to back it up.

I’m not saying this just because I am an insurance broker who has the appropriate academic credentials, I’m saying it as someone who is already seeing the fallout of the situation that Hall was talking about.

I mean it too when I say that you must choose your risk adviser carefully. The insurance industry, unfortunately, has gone down a path of cost-based business models. The profits that keep the industry functional are derived from how customers transfer risks, rather than from advice on how to mitigate risks. In this situation, when the cost base rises, the insurer margins get squeezed and we end up with an entire sector on a knife-edge. This is what is currently happening.

If you’re adapting, so must your insurance company

I would like to think that the insurance industry is shifting from that cost-based model to a service-based model built around well-informed risk advisers working with business managers to engage with risk. Yet, if this broad change is happening, it’s happening too slowly.

To be honest, most insurance brokers don’t possess any business acumen beyond what they’re required to have as part of their license to be an insurance broker. So, there is a degree of ignorance about risk management on both the customer’s side – you don’t know what to ask for – and on the supply side – your insurance providers don’t know what questions to ask.

Our philosophy: the answer can only be as good as the question you ask.

For insurance brokers like myself who have academic credentials in risk mitigation, our role is not to force business owners or managers to decide on how they choose to engage with risk. Our role is to provide data on what their exposures are and advise on the pathways towards mitigating these – whether the be operational changes or changes to a contract of insurance.

Good risk management is good business practice

To me, these issues all boil down to ‘what is the most cost-effective way to deal with this risk?’ Is it cheaper to transfer it to a contract of insurance? If so, fine. Is it cheaper to modify your business in some manner to reduce the risk long-term? If so, great! Ultimately, the latter should be your goal (within reason).

We are not here to use scare tactics, telling people everything that could go wrong in order to try to sell more insurance. When insurance brokers like us have ongoing relationships with our clients, we’re working with them to build a better, more stable and more resilient business overall.

Really, I am talking about giving risk resilience equal footing to profit margin in your business strategy. If your business is not risk-resilient, if it is brittle, then the profit margin doesn’t matter: you don’t have a stable operating base.

The business world of 2021 is in uncharted territory. The world is more connected, more dynamic and more surprising than ever. You can’t establish resilience in the new world by going for the cheapest quote generated under old-world assumptions. You have to be smarter than that.

You need insurance for many of the good things in life – travelling, running a business, buying your home, etc. These are all important things to protect from hazards, however no one teaches you how to buy the insurance to give you that protection. Especially not many of the insurers selling it.

When most of us – I’m including both consumers and businesses here – go to buy something, we look online for what we think is a good deal. We’re blissfully ignorant that taking this route can leave you high and dry if you need to make a claim. Even if you’re usually pretty switched on, you don’t know what you don’t know (we’ll get into that later).

So, if you’re thinking about buying insurance online but are worried about wasting thousands on a policy that won’t come through, this is an article for you.

Based on my 13 years as an insurance broker, these are the top three common mistakes people make when buying insurance online.

1. Putting The Wrong Business Name on the Application

Getting your name right on a form seems like primary school stuff, but people get it wrong on their insurance forms more than you can imagine. While a fat-fingered typo won’t necessarily be a deal-breaker, forgetting to add the correct business identifier or writing in something altogether different from your business name could be.

I’ve seen countless businesses that might have come undone because:

They’ve registered under the parent company’s name, but are trading under a different business name.

They’ve changed their business name, but the old name is still listed on their policy.

The name of the business they’re trading under is incorrectly listed in their policy documents, and actually describes another company with a similar name.

When scenarios like these come up, the result is usually a lively discussion between the policyholder, the insurer and sometimes the ombudsman about the purchaser’s “intent”.

If you bought the policy in good faith but under a technically “wrong” business name, you may still be able to claim, but is that an argument you want to have after you’ve just suffered a significant loss?

If you’ve used one business name instead of another because the business you’re actually trading under has a dubious past, the insurer will most likely not view that as good faith – more like deliberate non-disclosure. It’s very likely you can say goodbye to your claim, your cover and all the premiums you’ve been paying out!

What’s the easiest way to avoid this situation? Get advice someone you can trust!

2. Thinking Near Enough Is Good Enough When Listing Your Occupation

Drop-down menus catch a lot of businesses out when they’re applying for the regular forms of insurance, such as business insurance, public liability or professional indemnity.

Here’s how it happens:

The site asks you to choose your occupation from a drop-down menu.

Your exact business type is not listed, but there is one that seems close enough.

You pick that one.

You click “Buy”.

Congratulations, you just bought an insurance policy covering work you don’t do!

Case in point: I recently worked with a hi-tech cleaning company that microbially purifies business premises top to bottom. The business thought it was doing the right thing when buying insurance through a comparison website. Later, when the owner came to me to review the policy, I saw the business was categorised as carpet cleaning.

The business hygiene provider had already been operating for months. If an incident had occurred regarding any operations not related to carpet cleaning, then they wouldn’t have had any cover at all! Like any innovator, this business didn’t fit neatly into any of the standard menu options. We soon got their insurance sorted out through working directly with the insurer.

If you’re not sure if you’ve listed your occupation correctly, don’t be an ostrich. Pull your head out of the sand. Pick up the phone and ask your insurer to specifically note your occupational duties on the policy. If they won’t, there’s probably a good reason: they don’t cover those activities. Find an insurer who will or find someone who can help you get it right.

3. Relying On Comparison Websites For All Your Research

Comparing policies online might feel like due diligence, but comparison websites aren’t actually there to give you great protection; they’re designed to make money from referrals.

Here’s why comparison websites rarely offer business owners the best value:

They offer one-size-fits-all policies: Your business is (or should be) different from every other company in your industry. Your insurance has to reflect that. Comparison sites don’t give much opportunity to tailor a policy to your unique risk profile. This means most people who buy online either end up underinsured (i.e. with spotty coverage) or overinsured (i.e. paying excessive premiums).

The pool of insurers they draw from is tiny: As insurance brokers, we can access about 140 different insurers and thousands of policy wordings. As a consumer on a comparison website, you can only choose from maybe 6 to 10 different options. Plus, you have no way of knowing how the insurer you select responds to claims. We, on the other hand, know which insurers have a reputation for wriggling out of paying and which ones are known for behaving themselves when claims come up.

The devil is in the detail: It’s not always easy to know what you’re signing up for. Just like I have good knowledge about contracts but always get a lawyer to review mine, it’s always a good idea to get an insurance broker to review your policy before you sign it. At the very least, make sure you know the definitions, understand the policy limitations and are across the sub-limits.

A Simplistic Solution Usually Causes More Problems Later On

There is a big difference between simple and simplistic:

Something made simple still works properly

Something made simplistic doesn’t.

Buying business insurance can be a simple process if you have the right advice. But buying business insurance online is usually a simplistic process because you don’t have the right advice. You will pay good money for a piece of paper that says “policy”, but how much faith can you put in it?

Did you just bet your entire business on a policy you bought from a “Meerkat” after 10 minutes of clicking drop-down boxes with options that seemed close enough?

An online comparison site might be completely fine if you have a mainstream kind of business. However, if your business is an innovator or a little left-field – like the corporate hygienist in the example – you’re going to find plenty of things the comparison sites can’t do.

So, get your existing policy out or download all the details on the one you’re thinking of buying. If there is anything you don’t understand, that’s your trigger to call someone you trust to get an explanation.

My advice is that diving in and buying insurance without a good level of understanding is a not a good business risk to take.

The way I see it, your edge in business comes from controlling and consciously engaging with certain ‘good risks’ on an ongoing basis. It’s why I always say Risk-Reward-Repeat. The other side of this is that your business insurance is there to mitigate the bad risks.

So, don’t make buying your insurance a bad risk in the first place.

There is something I need to remind myself of almost every day and it’s not pretty: I’m ignorant. It’s not on purpose, I do what I can about it, and yet I will always have a level of ignorance. Just like everyone does.

Most of us travel through life cultivating a dusty collection of known-unknowns in the corners of our minds. You know the sort. I’m talking about those issues that if you can put full awareness on them, they trigger the mental response of: I don’t know and I don’t want to know.

But to tip the old saying on its head: what you don’t know can hurt you. And if you’re an entrepreneur, then that hurt will extend to your business.

Insurance is one effective way to mitigate the risks of these unknowns. The problems arise when your insurance is itself an unknown!

Many entrepreneurs place their insurance in the too-hard basket which is, honestly, understandable. The average insurance product description can be up to 50 pages and people – especially business owners – are time poor.

Nevertheless, staying ignorant about your insurance has routinely disastrous consequences. I see them every week.

Today, we’re going to delve into ignorance. Specifically,

the common sources of ignorance about insurance

the risks you take by keeping your head in the sand

how you can mitigate powerlessness through knowledge.

Do you know what insurance is? Are you sure?

A true understanding of insurance goes beyond knowing what’s in the contract you’ve signed. Insurance is, at its core, the holistic management of risk. I say ‘management’ here because risk isn’t always something to be avoided.

Properly managed risk can be the fuel that propels your business into future success. Often, this success is of a magnitude you could not have achieved if you had not taken that first ‘risky’ step.

The right insurance enables you to take such risks because it puts a net under the trapeze. If you fall, you have a safe place to land. Knowing this, you can swing out harder and reach higher without your creativity, passion and drive being hindered.

This is the real role of business insurance. Sadly, most people are ignorant of this fact – often, even insurers and brokers get it wrong. Many people see risk as something to be avoided altogether. They focus so hard on what happens after a claim that they fail to manage the risk factors that lead up to it.

Luckily, this kind of ignorance is easily fixed. The crucial first step is to start seeing your insurance as more than just crash protection. Instead, see your insurance as ‘risk management’. Make rational engagement with risk into a tangible element of your business strategy.

And it goes without saying, get yourself an insurance broker who respects the role of risk as a key ingredient in a successful business.

Insurance premiums too good to be true? They probably are.

Insurance companies are not charities. They’re there to provide cover that’s fair, reasonable, and priced accordingly. Higher risk equals higher price – it seems so obvious.

However, I see many cases where a business’s premiums were too low and they only found out what this means when the time came to put in a claim. They suddenly face the fact that low premiums meant there were gaps in their cover. Sometimes these gaps are so big the whole business can fall through.

Conversely, if your premiums are too high it’s also a red flag. Either:

You don’t fully understand the risks associated with your business

Your insurer doesn’t understand your business’s risks, and you’re losing money, which, I think we can all agree, is never a good thing!

It can be all too easy to ignore the numbers when it comes to insurance, particularly if you feel like you’re getting bargain rates. But maintaining this particular ignorance is often catastrophic.

Businesses routinely collapse because something fairly mundane has happened whose risk they had not mitigated and which wasn’t properly covered by their insurance. It’s essential that you learn the risks associated with running your company and ensure your insurance covers them all.

If you’re unsure how much your business ought to be charged for insurance, a good preliminary check is to gather up advice from a handful of providers and brokers. I’ll happily be part of your round up.

Anyway, if their quotes don’t match what you’re currently paying, then you should work to patch the proverbial leak before it becomes a flood.

Examining your ignorance is more rewarding than you might think

Everyone is ignorant of something. None of us knows everything. It’s impossible. There’s a certain power to accepting this truth and working with it.

By examining your own confirmation bias, you’re not only mitigating the risks your company might face, you’re also giving yourself the power to strengthen your business practices. Being well-versed in risk gives you the confidence to make decisions you might otherwise shy away from. And it’s those risky decisions that make for a groundbreaking business.

Not to imply that facing your own ignorance is easy. Becoming suddenly aware of all the risks your business faces can seem like you’ve walked into a den of sleeping wolves with nothing but brittle twigs underfoot.

However, you already know that discomfort is essential for growth. Once you’re able to reframe your response, the power to be gained from your new knowledge will make the growing pains worth it.

Business insurance still the monster under your bed?

Still unsure about your business insurance? That’s fine too. The most successful entrepreneurs achieve so much because they are acutely aware of the limits of their knowledge and understand the value of engaging experts to fill those gaps. They are powerful people because they engage with their ignorance strategically.

Insurance brokers like me make it our business to understand your company – the ins, outs, ups, and downs. At Alleviate Risk we go the extra mile by focusing not only on the outcome of claims, but also the risk factors that lead up to them. Because the best incident is the one you avoid altogether.

“Risk-Reward-Repeat” is our slogan for a reason. We understand insurance for our clients so they reap the rewards of carefully managed risk.

When many parents walk into a child’s play centre, they relish the rare opportunity to let their little ones run wild and free. As an insurance broker and a parent, when I drop into my local centre with the kids in tow, I look around at the organised chaos and my imagination starts racing: Lawsuits! Litigants! Liabilities!

I was approached last year by Stacy and Des MacKellar just after they’d bought the Chipmunks Playland & Cafe franchise at Sippy Downs, Queensland. Their business, which spans a few hundred square-metres of play equipment in a fully contained all-weather building, was an opportunity to really flex my risk-mitigation muscles.

While the MacKellars were already fastidious about health and safety and had all the regular bases covered (literally, with foam and matting), I wanted to help them mitigate the few risks they hadn’t anticipated.

Chipmunks Owner Stacy MacKellar (left) and Manager CiCi MacMillan

Just a few months after they’d officially signed on with me at Alleviate Risk, my advice was put to the test in a big way: an incident occurred involving the child of an allied healthcare professional visiting the centre. She claimed her child had suffered a spinal injury on the slippery slide.

It’s the sort of allegation that can destroy an underprepared business if it’s found to have legal standing in court! But that’s not what happened here.

Read on for how it all played out … and how I can help you benefit through professional risk management.

When It Came to Child Safety, The MacKellars Already Knew A Lot

After a 20-year career as a police officer working largely in child protection, Des MacKellar had witnessed first-hand what can go wrong when kids’ safety isn’t prioritised. He’d dealt with some horrible cases and leant on his family and his passion for preserving human life to cope.

Stacy’s background is in small business. She came from a family that has always owned enterprises. She’d grown up around businesses, worked in finance and insurance, and, from the first phone call, let me know she understood the importance of tackling risk exposure.

So, when their local Chipmunks play centre came up for sale, the couple’s diverse experience meant they were perfect buyers to operate it this demanding sector. Why?

Both policing and the business/finance sector are highly structured, procedure-heavy and sometimes litigious. Further, running the play centre would allow the MacKellars to build on their skills while dialling down on the stress and boredom of their previous occupations.

You’re probably wondering, why did these procedure and safety gurus need my help?

High Premiums Or Risk Management: A No-Brainer

Today, Chipmunks Playland & Cafe Sippy Downs has up to 10,000 visitors per week – as many as 250 kids are running around and playing on the swings, slides and jungle-jims at any one time. With that many kids, each with different levels of social and physical development all concentrated in one place, Stacy and Des knew there would be run-ins.

They weren’t satisfied, however, with simply paying high premiums to insurers who offered them one-size-fits-all policies that only factored worst-case scenarios into their premiums. The MacKellars wanted real risk management, not just renewal notices.

Yes, they had accepted that bumped heads, grazes and even occasional ambulance calls were common in their industry, but they were still determined to find ways to make their centre genuinely safer. This would, in turn, reduce their premiums because they’d mitigated as many risks as possible.

The Best Price By Preparing For The Worst Outcome

I still remember what I said to Stacy and Des when I first inspected their premises.

“Someone is going to try to sue you, not because you’re bad operators, but just because of the nature of the business itself.

“Sooner or later, you’re going to be put under the microscope. We have to make sure you get gold medals when that happens.”

Those are not pleasant words for any business owner to hear, but they can be the difference between litigation destroying your business or a successfully defended claim showing your strength in the industry. Stacy and Des knew where I was coming from.

Once I’d completed my report, I told the MacKellars I’d identified three simple things they could do to protect themselves straight away:

1. Cameras: The Antidote To Anecdotal Evidence

The Chipmunks’ staff are not childcare workers: they are there to supervise and maintain the equipment, not manage the children. So, the first thing I instructed the MacKellars to do was get cameras to record every square-metre of floor space.

They did just that, installing cameras in the play centre and linking them to their mobile phones for quick access to all the footage. This would prove to be a particularly smart move, as they’d later be able to provide evidence of exactly if and how injuries were sustained, and, by doing so, disprove any fabricated stories.

2. Documentation: The Best Friend Of The Facts

Incident reports are vital tools for every business. Not only do they help you identify, at a ground-level, areas that pose risks to customers and staff, they are also crucial for businesses that end up having to defend themselves against a personal injury claim.

Here’s what Stacy has to say about her relationship with documentation and reporting:

“Yes, you feel like you’re constantly writing and note-taking. We say to staff: if it happens, put it in the diary. Times, dates, names and details of anything notable or concerning. Taking notes: it is going to protect you! Document, document, document!”

3. Culture: Your Staff Are Your Best Risk-Protection Tool

Although Des and Stacy understood the importance of child safety better than most, their staff (often teenagers with no kids of their own) were an untapped resource for identifying and mitigating risks.

Not content with just training staff on simple procedures like checking equipment, sanitising surfaces and documenting incidents, Stacy and Des wanted to show their insurers and customers that their Chipmunks franchise represented the gold standard in safety.

This meant implementing additional risk-reduction policies that went beyond legislative requirements, including:

Ensuring all staff teams had a senior member over 18 years old present at all times

Having at least one first-aid trained staff member on the floor at all times

Hiring managers who have childcare certifications (even though they aren’t required to do so).

By training staff to employ the best policies and procedures in the industry, the MacKellars were able to mitigate risks far more effectively than their peers. Simply, they’d be able to say to insurers or litigants: “What more could we possibly do?”

The Infamous Slide Incident

The slide at Chipmunks Playland Sippy Downs

All of these risk-mitigation strategies came into play one day on the slide. What happened was fairly straightforward:

An incident on the slide occurred involving an unsupervised child around 10 years old.

The child’s mother did not see the incident.

Around 40 minutes later, an off-duty staff member was the first to notice something wrong.

The centre’s management was immediately notified.

The mother then made a complaint, saying her child’s back had been injured.

The mother called an ambulance.

The ambulance arrived and examined the child.

It was at this point that on-duty Chipmunks’ staff were told the child had been complaining of tingling and neurological signs. However, the child was also on medication for several pre-existing developmental and psychiatric conditions – all of which could also have been responsible for the symptoms.

The ambulance paramedic said they couldn’t diagnose on the spot, and felt there wasn’t an injury significant enough to warrant a trip to the hospital. The mother insisted they go anyway. The hospital declined to check in or admit the child, and the mother’s request for a letter from the doctor was refused on the grounds that nothing was wrong with her child. The child was given supermarket-grade painkillers and sent home.

The next day, Chipmunks followed up in order to complete their incident reporting procedures and inform the mother that they had video footage which had been reviewed.

Furthermore, they let her know that it was within their policy to not only call an ambulance when necessary (as she had done) but to section off and inspect the area where the potential injury had occurred before it is used again (which they had done). Neither the footage nor the equipment supported the mother’s version of events leading up to Point 5 above.

Upon hearing this, the mother relented and signed the Chipmunks’ incident report, saying:

‘I hope you have us back, you probably think we made this all up.’

How Did Our Risk Mitigation Help Chipmunks In This Incident?

While the MacKellars’ facility already met Australian safety standards (they also have all equipment, fencing and play areas independently tested by independent consultants DRA Safety), Des and Stacy could have been in big trouble if they hadn’t been so proactive in other ways.

By introducing a constant safety feedback loop between staff, management and insurers, they were able to begin managing the issue instantly, back their safety claims with evidence, and get a written incident report signed by the mother.

All this was then sent to me straight away, and I passed it on to their insurer to let them know a claim might be imminent.

Insurers actually welcome information like this.By flagging incidents, the clients of insurers demonstrate that they understand, mitigate and manage risk instead of passing all the exposures on to be insured. And, the client and the insurer both know they’ll be backed by solid evidence if an incident ever does make it to court.

With this kind of heavy interaction, the insurer is a lot more comfortable knowing their relationship is being managed. In my experience, comfortable insurers are good insurers.

How Do I Mitigate Risks?

Obviously, my answer would be, “Hire me, Morgan Appleby, to be your insurance broker! I’ll help you identify and mitigate risks!”

But, instead of it coming from me, I’ll let Stacy do the talking:

“I chose Morgan independently and I’d absolutely do that 100 times over. We are in regular contact with him. He sends us his newsletter and any other random things he comes across that are relevant to us. We are very grateful that he is in our corner.

“We control those things we know we can control. As for everything else, we have insurance – it protects us as a family and a business with staff and patrons.”

If that sounds like what you want in your insurance, call me. At the very least, I’ll give you a few pointers on common pitfalls in your industry. At best, you’ll be managing risks, keeping more money in your pocket and accessing better insurance.

Every business move or investment has risks, it’s why it also has rewards.Manage things well and you’ll be able to repeatedly enjoy those rewards while being covered for the risks.

As a tertiary-educated risk-mitigation expert (and fellow entrepreneur), I can help you do all this effectively, just email me at morgan.appleby@alleviate.insure.

By Morgan Appleby,MBA, Grad. Dip Bus. Admin, Dip. Fin. Serv. (Broking)

Don’t listen to what the economists say. We humans are not rational creatures. Our mental blindspots are huge and we’re prey to literally hundreds of cognitive biases.

These affect any decisions made by anyone – from our most level-headed leaders right through to the tinfoil-hat-wearing illiterati.

One of the most insidious of these maladaptive influences is confirmation bias.

‘But I don’t have confirmation bias! I’m as balanced as they come!’ I hear you say.

To which I reply, ‘Your belief in your lack of confirmation bias merely confirms your bias towards believing in your own imperviousness to bias’.

While pointing out confirmation biases rarely wins me friends, it’s a worthwhile exercise when you’re an insurance professional, because confirmation bias poses a serious threat to businesses.

Are you aware of how your mental tendency to agree with yourself impairs your company? Let’s look at the whole issue a bit closer.

What is Confirmation Bias?

Simply put, confirmation bias is the tendency to look for and overvalue information that supports your existing beliefs (which, by the way, may or may not be rational), while simultaneously downplaying information that contradicts those beliefs.

The reality is that you, me and anyone else is wrong about a lot of things a lot of the time. And ill-informed decision making rarely garners ideal results.

Here are three ways confirmation bias might be affecting the business decisions you make:

1. Assuming Your Opinions are Factual

The less you know about any given subject, the more likely you are to have a stronger unconscious bias towards believing you’re right about it. And the stronger your biases, the more likely you are to make an ill-informed decision.

Smart people are unusually susceptible to this. How? Let’s take the example of a talented doctor working in a hospital. She’s an expert in her own field and has become very good at backing herself. Medicine is the only career path she’s tried and she’s been highly successful. She’s worked hard and everything has gone right so far.

Therefore, she has a subconscious bias that she’ll enjoy the same success when she decides to leave the hospital and launch herself as an independent general practitioner. However, she hasn’t put anywhere near the same time, effort and money into running businesses as she put into becoming a great doctor.

She opens her GP office and things don’t go well. Yes, she’s working hard and giving quality care. She thinks she’s doing everything right, but her business just can’t catch a break for some reason.

She doesn’t know she has the confirmation bias blinkers on. Instead of perceiving the actual factors governing her business success, she works harder and harder and longer and longer hours. The business still haemorrhages money. Eventually it collapses.

To the end she still believed she was doing everything right and, simply, not working hard enough.

2. The Boss Is Always Right (Except When They’re Wrong)

Many business owners I know love the old adage ‘if it ain’t broke, don’t fix it’ because a big part of their role is ruthlessly prioritising what is broke. However, just because you think you can accurately prioritise issues within your company, doesn’t mean you’re actually doing it.

It can be really hard to take heed when people who have no vested interest in whether you succeed or fail point out some flaw in your operations.

Frontline staff are also often the first to detect a problem within a company, yet just as often they don’t want to risk telling the boss something he or she won’t want to hear. Instead of raising an issue they:

Let small problems silently grow into big ones

Create their own inefficient solutions to the problems

Skew the information they provide to management in order to make things look rosier than they really are.

By the time the problem becomes obvious to the boss, it can be too late. Everyone in senior management is blindsided and left wondering, ‘How did this go so wrong so fast!’

It went wrong when management believed its own assumption that problems it wasn’t seeing didn’t exist.

3. Past Performance Is Not An Indicator Of Future Performance

You’ve probably heard this at the end of every superannuation commercial, but have you ever stopped to consider the implications it has for your business?

One of the greatest confirmation biases that business owners face is assuming that because their business has done well in the past it is prepared to do well in the future.

Professor Raymond Nickerson, the world’s leading confirmation bias researcher, explains our tendency to preference conclusions we make early on in our business journey:

“When a person must draw a conclusion on the basis of information acquired and integrated over time, the information acquired early in the process is likely to carry more weight than that acquired later.”

Thus, we over-value the way we did things when business was going well. Just because your business experienced growth last year, it doesn’t mean you were the main factor in that growth or that the growth will naturally continue this year.

How Confirmation Bias Works And Why We All Have It

Don’t think that confirmation bias is just ego taking over. Although overconfidence plays a large role in many poor business decisions, the root cause of confirmation bias harkens back to the fight or flight response our primitive ancestors needed to stay alive.

Early humans used cognitive-processing shortcuts like fight or flight to quickly and efficiently respond to life or death circumstances.

With the stakes so high, it was always better to err on the side of caution: privileging harmful past experiences over careful evaluation of the information at hand. After all, it is better to mistake a thousand trees for a tiger and run away than to mistake one tiger for a tree and stand still!

Today the threat of being eaten alive has all but disappeared, yet the cognitive survival mechanisms that resulted from about a million years of facing such risks are still hard-wired into us. They still govern much of our day-to-day decision making.

How You Can Protect Your Business From Your Biases

The good news is there are steps to take to mitigate the negative effects of your cognitive biases for your business. Here are four:

1. Acknowledge Your Biases

Confirmation bias is particularly problematic when you either:

Genuinely don’t know it is influencing you

Believe you can’t be influenced in the first place.

As they say in AA, ‘acknowledging you have a problem is the first step’. Only when you’re aware of the role confirmation bias plays in your life can you begin to work within its effects.

No, you’ll never be able to completely quash your biases. But, if you can be a little more aware of yours than your competitors are of theirs, you’ll be 10 streets ahead.

Ironically, you have to admit how vulnerable you are in order to reduce your vulnerability.

2. Collaborate With Independent Third Parties

As an insurance broker, I have the privilege of seeing how many different businesses in many different industries operate.

It’s my job to learn the ins-and-outs of these businesses so that I can offer accurate risk advice to owners who, while exceptional at what they do, can often no longer see the forest for the trees. Often, I have uncomfortable things to say.

The business owners who continue to thrive after I’ve come on board tend to be those who fully embrace a collaborative approach.

To put it plainly, it is easier to see someone else’s biases than it is to see your own. By allowing fresh eyes to take a look at your business, you’ll recognise the blindspots that your own cognitive biases have caused.

3. Encourage Dissent

Yep, you should actively seek out opinions, attitudes and beliefs that are uncomfortable. It’s very healthy for your staff to feel comfortable speaking out. Dissent in the ranks is exactly what leaders need when a tiger is picking off troops in the rear.

Don’t let a belief in your own superior business acumen or a fear of being undermined cloud your judgement. Great leaders are receptive to criticism and questioning. They encourage critical analysis. This is how they ensure that their company’s culture is free from the toxic, compounding effects of confirmation bias.

The human brain is naturally lazy. Combatting this laziness with intentional critical thinking is one of the most effective ways to fend off the negative effects of confirmation biases.

The next time you’re in the middle of a conversation and someone makes a statement you don’t agree with, have the insight to stop and ask yourself why you don’t agree.

Is it simply because you have an alternative opinion, or are you privy to factual information the other party isn’t?

Do you have a preconceived bias on that particular subject?

If so, where does that bias stem from?

Train your brain to ask these questions and you will become more self-aware and less susceptible to unconscious bias (just don’t start thinking you’re completely infallible!).

The Bottom Line

There is a Mark Twain quote I come back to almost every day:

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.

Because of the way human brains have developed, we all have confirmation bias. How you deal with your personal biases has a huge effect on your business.

Ignore them or refuse to acknowledge their existence and you’ll be exposed to risks that could destroy you.

Accept that your decision making is influenced by invisible biases then learn how to counter them, and you’ll be able to take risks your competitors think are too ‘risky’. You’ll be able to repeat successes they couldn’t pull off even once. And you’ll reap rewards while they languish in ill-informed decisions.

In my field, the simplest proof that defying your confirmation bias works happens when I advise a client to get cover against a certain kind of incident.

I can see how their growth is continually ramping up its probability, but their confirmation bias means they can’t see this. You’d be amazed how often the incident happens within 18 months.

The choice to confront your cognitive shortcomings is yours. If you’re ready to have your eyes opened to more of the bigger picture, drop me a line at morgan.appleby@alleviate.insure or call 1300 253 848.

This article is for people who don’t understand business insurance, but need to. This usually means you’re in business yourself. And, if you’re in business already, then you probably already have the main thing you need to make enough sense of the whole topic of business insurance: instincts. There are two major business instincts relevant here:

Business Instinct A: Am I getting a fair deal?

Business Instinct B: Do I know enough to know if I’m getting a fair deal?

In this article, I’m going to cover the basics of business insurance so that when you’re ready to get cover, you’ll have your bearings and know the right questions to ask. I’m going to fill you in on a bit of B so you have a sharper instinct A.

What is insurance?

In short, insurance is a promise (contract) between you and your insurer wherein you both agree that if an “insurable event” happens to you in the next 365 days and you’ve paid your premiums (a fixed cost outlined in your contract), the insurer will pay you a certain amount of money to cover your losses.

However, as you might have guessed, not all promises are alike. The types of events that you can be insured against, the amount of money you have to pay your insurer every billing period, and what you can claim if the worst happens will all vary according to which insurer, policy and type of insurance you take out.

No insurance policy will ever cover every risk associated with running a business. Not only is it impossible to plan for every single thing that might happen to your company, but even if an insurer could do that their premiums would be through the roof.

This is where prudent advice and good risk management come into play. A good insurance broker will study and understand your business. Once they have a good grasp on your revenue streams, they’ll be able to explain in depth:

the cover you have

the cover you need

the cover you can probably do without.

Most importantly they will be able to tell which of your risks are uninsurable.

Then, if they’re qualified or educated to do so through some form of academic qualifications in risk management, they’ll also guide you through setting up procedures in your business to try to alleviate some of the unknowns to help keep your insurance premiums reasonable and sustainable.

How insurers decide the value of a policy

Insurance companies rely on specialists called actuaries to calculate the risks in a specific occupation or industry.

Actuaries study every single detail of a business operation and then use algorithmic models to calculate insurance premiums. For example, an actuary at a sawmill will consider many factors including (but by no means limited to):

Geographic business location

Type of timber

Age of equipment

Staff training

Construction of the business facility

Nearby emergency services support

Local environment

Historical industry data on prior claims.

Once they have these and hundreds more data points, the actuary gets number crunching. From their findings, they then advise the insurers as to what the risk profile of the operation is. Using this information, the insurer can work out what a profitable yet fair insurance premium would look like and what their policy will and will not cover.

The 7 types of insurance your business might need

Many businesses underestimate how much risk they’re exposed to every day. While most business people are aware that their company could be affected by a fire, burglary, flooding, equipment breakdowns or some kind of accident, they don’t realise that there are many other very real threats they should insure against. Let’s look at a few:

Professional liability insurance: If you’re a professional, chances are that a mistake you make could cause one of your clients financial loss – and those are the type of mistakes that preface lawsuits. This insurance isn’t just for doctors or lawyers, however. Even a marketing professional who is responsible for a brand’s image should consider taking out professional liability insurance. If you’re good at what you do, chances of a claim is unlikely. The problem is that it’s usually the legal defence costs that result in a higher expense that the actual financial loss itself.

Product liability insurance: What would you do if a product you manufacture causes property damage, injures or even kills a consumer? If you have product liability insurance, you can rest assured knowing that a personal injury or property damage lawsuit won’t destroy your business. A common misunderstanding in product-type exposures are your obligations under Australian law. In short, if you import anything for ‘resale’ under our legislation, you are deemed to be the ‘manufacturer’ of that product.

Public liability insurance: Does your business interact with the public? If so, you need to know that in the event that someone is injured or their property is damaged while you’re providing your services, you could be liable to cover their losses. Public liability insurance is designed to protect you from this.

Property insurance: Anyone whose business is located within a specific physical premises needs property insurance. This type of insurance is designed to ensure that both the building you operate out of and the equipment and inventory within it are covered in the event of a fire, flood or break-in.

WorkCover: Every Queensland business that employs workers is legally obligated to insure against workplace accidents with a WorkCover policy. Other jurisdictions have similar regulations.

Business interruption insurance: How long could your business survive an unexpected interruption to trade? One week? One month? One year? This type of insurance can help contribute to your cash flow if you experience a loss of revenue, a loss of name and good fame, or some other event that interrupts trade.

Car insurance: Taking out a policy for your work vehicles is a no-brainer. You insure your family car, so why wouldn’t you do the same for your business cars?

How business insurance differs from personal insurance

First up: personal insurance policies are a lot simpler than business policies. While people who don’t own businesses simply need to insure tangible assets like their income and property, business owners must insure both tangible and intangible assets (such as loss of trade).

For example, consider the many questions that must be asked when a loss of trade claim is being evaluated:

Who/what is responsible for the loss of trade?

Has the business also suffered a loss of reputation?

Are there measurable lost opportunities?

Is the business’s revenue straightforward and easy to average, or do recent records include windfalls?

Will purchases need to be made to restore the business to its former earning capacity?

How much revenue will be lost until those purchases are made?

How do each of these factors affect the other factors?

The more business insurance research you do, the more you realise how irreducibly complex your business is! There are so many different cogs in the machine, and they must all work together for you to make a safely insurable profit.

If your livelihood hinges upon your business working smoothly every day, I cannot overstate how important it is that you have a backup plan for if/when one of these cogs conks out!

5 tips for making your business more insurable

When it comes to buying insurance for your business, there are steps you can take to get access to more cheaper premiums. If you want the most competitive offers on the market, it’s a good idea to:

Mitigate risks: Have policies and procedures (safety training, risk management reviews, etc.) in place that reduce the likelihood of an incident happening in the first place. This is often the best and cheapest form of ‘insurance’ possible.

Improve security around your business: Installing alarms, cameras, sprinklers, digital security protocols and other security products may be a significant short-term cost to your business, but this can help you save a lot on your premiums over the long term.

Bundle your insurance: If you own multiple businesses, you may be able to get a better deal by insuring them all under one company. Just make sure that each policy provides adequate, tailored coverage for its corresponding business.

Pay in advance: As with health and vehicle insurance, you’ll pay more if you opt to pay monthly. If you can, pay your premiums for the whole year in one go.

Use a broker: Cheap insurance isn’t always good insurance, so unless you enjoy reading fine print and studying industry jargon, it’s a good idea to find an independent broker who will do the research and bargaining for you.

How you can invalidate your business insurance policy

When you take out a standard business insurance policy, you can rightfully then expect to be provided with 12 months of cover. There are, however, certain circumstances that can invalidate your insurance policy. These include:

Failure to pay premiums: If you miss a payment you may not be covered until you’re caught up again.

Deception (deliberate or accidental): If you make a false statement (whether deliberately or accidentally) about one or more aspects of your business during your application process, not only will this deception affect whether your future claims will be paid out, you may also find yourself in trouble with the law! You must always be honest with your insurer and disclose all relevant information. The rule of thumb here: if you’re not sure, get advice.

Illegal activities: In the event your business incurs a loss because of your criminal behaviour, don’t expect your insurer to pick up the slack.

In addition to these definite deal-breakers, most policies will include other exclusions. It’s important to understand what your policy will and won’t cover.

Don’t be afraid to ask your insurance broker or the insurer themselves very specific ‘what if’ questions. It’s better to pay a little bit more for the cover you need than to be paying low premiums for a policy that won’t help you out when you really need it!

Business insurance 101

So there you have it, the basics of business insurance. We have looked at what insurance really is and touched on how insurers go about offering it.

You now have a grounding in the basic types of business insurance and how the field differs from personal insurance. And last, we touched on ways you can make your business more insurable … plus a few things you can do to make it much, much less insurable.

All that lot should be enough to satisfy Business Instinct B (knowing enough to make the next step) as mentioned back in the introduction. So, what is the next step that’s going to start exercising Business Instinct A? Find an insurer or insurance broker to apply all the concepts we have talked about to your specific situation.

Get the risks right, and you’ll be able to safely repeat them … and reap the rewards. Want to know more about how business insurance is a crucial gateway to growth? Drop me a line: morgan.appleby@alleviate.insure